Equity, also known as stock, represents a claim of ownership of the assets and earnings of a company. Companies typically grant stock options that, if conditions are met, can be converted into company shares. When this happens, the contractor becomes a stockholder.

The benefits of giving equity to contractors

- Equity incentivizes contractors to renew their independent contractor agreements instead of looking for new clients

- Equity allows contractors to reap some of the value they’ve helped create

- Equity is less expensive for early-stage startups to give as compensation since its true value accumulates over time

- Companies can gain access to the talent they would otherwise be unable to afford by partly paying them with equity

The disadvantages of giving equity to contractors

The disadvantages of equity compensation for contractors and hiring companies are as follows:

- Since contractors often have multiple clients, giving them stock options may create a conflict of interest. You’ll need to clear this up in advance of issuing them options

- Venture capitalists (VCs) prefer it when your cap table has many long-term employees. Distributing stock options among contractors carries the risk of dead equity—a situation when stock is owed to someone who isn’t involved in the business anymore. This can create headaches for VCs who would like to buy more of your company down the line

- For the business relationship to make sense and ensure compliance, more protections and clauses are necessary for equity agreements with contractors. Since contractors often work on a short-term or project-by-project basis, putting in place mechanisms like vesting schedules, for example, is often unnecessary and might give rise to a perception that the contractor is a misclassified employee.

This article will guide you through the steps in providing contractors with equity.

Disclaimer: This content does not constitute legal advice. Please consult a legal professional for guidance on your specific case.

Step one: Decide on the best types of stock options for your contractors

The type of equity you choose to provide to contractors will depend on the stage of the company, whether you have raised a priced round during an external 409A valuation, and where your contractors are located.

The different types of equity are as follows:

- NSOs: Non-qualified stock options—companies tend to offer NSOs to international contractors during any stage of the company’s growth

- RTUs: Restricted token units (Crypto)—companies may choose to provide contractors with cryptocurrency during any stage of company growth

- RSUs: Restricted stock units—companies usually issue these to contractors at any stage of company growth

- SARs: Share appreciation rights—Companies offer these to contractors to enable them to receive the increase in value of a company’s stock over a set period

- ISOs: Incentive stock options— Companies should avoid issuing these to contractors since they entail tax obligations specific to employees and could result in a misclassification risk

- Gifting: While gifting shares is a rare occurrence made by super early-stage companies, it is possible to give shares to contractors

See also: How to Grant Stock Options to Foreign Employees

Step two: Decide how much equity to give to contractors

Once you’ve settled on the type of equity you want to provide, you need to decide how much equity to give to contractors.

How much will depend on numerous factors such as:

- The stage of your company

- The fair market value of the company and value of the stock (which changes over time)

- The contractor’s experience or performance

- The length of the relationship

- The level of risk involved

Determining equity stakes for contractors can be more challenging than for employees. Unlike employees, contractors are usually hired for a specific project or designated period. Their commitment level will differ, and your control over their work will be significantly less.

For each contractor, try to set your baseline as the minimum amount you need to offer that contractor to incentivize them. With that in mind, you’ll also need to consider that equity has more of a risk factor than cash incentives. The percentage you ultimately land upon depends on how valuable the contractor’s work is to your company and the market demand for their skillset.

Hiring independent contractors can help with that. And Deel can keep them from misclassification.

Step three: Choose how to structure equity incentives

The next step is to devise a stock option plan to structure your equity incentives so they benefit both the contractor and the company.

Here are a few common equity structures for contractors:

- Time-based: The contractor earns equity over a fixed period of time (typically in years) with a specific percentage vested at each date. This is the most common approach.

- Milestone-based: Equity is earned based on the contractor achieving certain milestones. For a salesperson, the milestone could be a certain sales target. For a software engineer, it could be a specific release date of the company’s product.

The best structure will depend on the contractor’s lifecycle and the complexity level you’re willing to take on. For example, a milestone structure is harder to implement since contractors typically work in shorter cycles. You’d need to define product delivery, which can be more ambiguous from a legal standpoint.

.png?width=1200&height=627&name=Equity%20(1200x628px%20-%20LI_IG_FB).png)

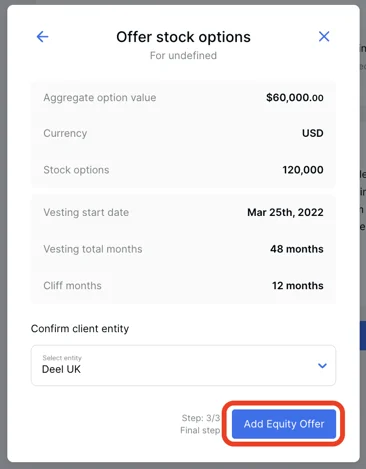

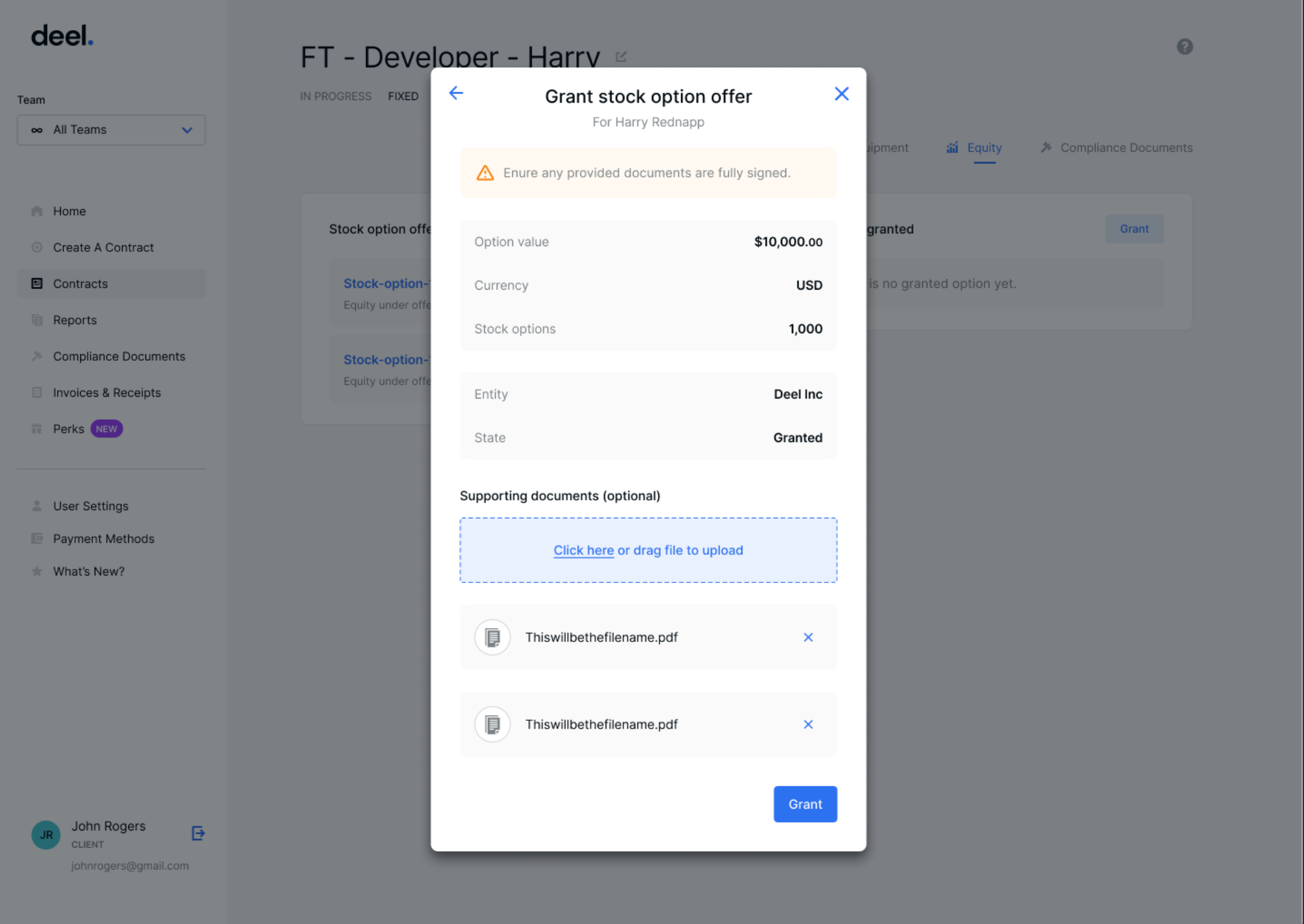

Step four: Draft an equity agreement, also known as a stock option grant

Once you’ve worked out all the details, it’s time to devise an equity agreement that discloses the contractor’s rights to purchase equity at your company.

An equity agreement should include the following components:

- The type of equity they’re getting

- The number of shares granted

- Their strike price (or exercise price)

- The vesting schedule (or vesting period)

- Whether early exercise is allowed

- How their shares are affected by acquisition or termination

- Any restrictions on the selling of equity

- The tax implications of exercising (and selling shares)

- The terms and conditions of the service arrangement that will result in a grant of equity to the contractor

- Their post-termination exercise window

- How to protect confidential information

- Which terms survive the agreement

- An arbitration clause if a dispute arises under the agreement

- The governing jurisdiction. Often the jurisdiction in which the company operates. However, this will vary for global companies

Step five: Educate your contractors

It is up to the contractor to determine whether they will give up some of their money in return for company equity. And for many, equity will likely be a new topic, full of new and complicated terms and concepts.

Before a contractor accepts and signs their equity grant, they’ll need to know what it is, how it could benefit them, and how purchasing equity could impact their tax treatment and financial standing.

Equity without the right context can be counterproductive because the economic benefit of ownership (especially with private companies) isn’t intuitively obvious.

For a baseline level of knowledge, contractors need to understand the following:

- All equity involves risk. If a company fails or gets acquired at an unfavorable valuation, then its shares may not end up with much or any value

- A diversified portfolio is the safest. Investing too much money in the company can lead to non-optimized decision-making

- Tax responsibilities increase. Depending on the type of shares, and tax rate, different tax treatments will apply to income tax and long-term capital gains

The potential upside. Based on the strike price and the company’s current valuation, what kind of value a contractor expect to see during a liquidity event

With the right education, getting equity means getting a potentially valuable asset that can bring contractors significant long-term financial benefits. Without it, it can mean missed opportunities and tax consequences.

Companies should compile educational resources to help their contractors understand the terminology, processes, clauses, and obligations.

Step six: Fulfil your tax reporting obligations

Providing company equity can result in a taxable event for the contractor and form filing responsibilities for the company, depending on the type of equity awarded and the contractor’s country of tax residence.

In the US, for example, if the fair market value of the shares increases from the exercise price in the initial share award to the contractor, the contractor must pay taxes under the alternative minimum tax regime (AMT).

If the US contractor can exercise their shares early, the contractor must submit a copy of form 83(b) to the Internal Revenue Service (IRS) and the company; the company must retain a physical copy.

The company must also file other IRS forms in other scenarios, for example, when it has issued $10m in options in one calendar year.

If the fair market value remained the same as the exercise price when the company granted the shares, there is no taxable event.

If a company “gifts” a contractor shares, this is a taxable event. The company must distribute the correct tax forms so that the contractor can report these earnings as miscellaneous income. This process is the same for most countries.

Grant contractors equity with Deel

For legal, finance, and HR teams, navigating equity locally and internationally can be complex, with regulations varying between jurisdictions.

With the help of our team, you can offer competitive incentives to your employees and contractors all over the world in various forms of equity or token grants. Our local experts work to secure an optimal legal and tax framework for Deel clients, providing guidance around handling all applicable taxes and withholdings, and assisting with reporting requirements.

Whether you have general questions about equity compliance or need help navigating new global equity options, our experts are here to help. Get in touch with our team today.