Compliantly hire independent contractors in Colombia within minutes

We automate everything in one account, from signing contracts and collecting tax forms to paying your global team. Deel partners with top legal experts in Colombia to ensure you’re compliant with local laws.

Avoid expensive misclassification mistakes in Colombia

Looking to grow your business in a new country and tap into a wider pool of talent? Hiring an independent contractor's a great way to go. You could run the risk of fines and penalties if you don't correctly classify a contractor since Colombia treats contractors differently than a full-time employees.

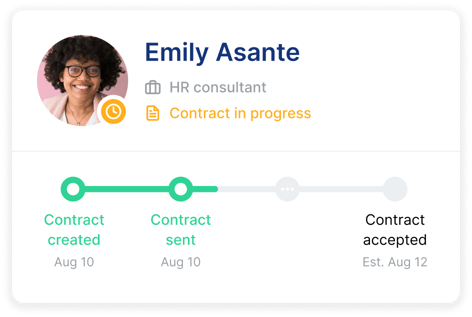

Quickly bring on contractors in Colombia

Just log into your Deel account and onboard independent contractors in Colombia within minutes. We'll make sure you're compliant and manage everything from localized contracts and collecting tax documents to international payroll.

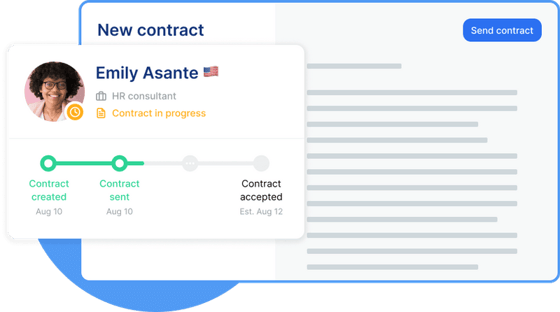

The best legal firms in Colombia ensure you're always compliant

The best legal firms in Colombia approve our contracts, assuring everything's compliant with local laws. From minimum wage and national holidays to termination conditions, you can be confident you have the most accurate and up-to-date information.

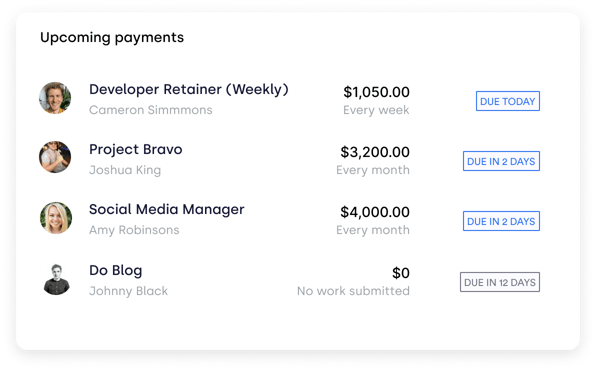

Fund payroll with one click in Colombia

Use your preferred payment method to send mass payouts in 120 currencies with just a click. Teams can also choose to withdraw money using their preferred payment method. Everyone saves on currency conversions and wire transfer fees. It's a win-win for everyone.

Our guide to setting up as an independent contractor in Colombia

Are you interested in the process of becoming an independent contractor in Colombia? We created a detailed guide outlining the registration process, documentation required, as well as the taxation system in Colombia take a look.