Today’s companies have unprecedented access to the world’s best talent. Thanks to remote technology (and the normalization of remote work), companies can hire independent contractors and manage remote workers worldwide: a company in the US can collaborate with freelancers in Argentina, Japan, South Africa, or Spain. And tapping into an international talent pool can transform your company, no matter your industry.

Job boards like LinkedIn and Upwork simplify finding contractors. But many business owners don't realize the legal considerations when hiring contractors, especially across borders. Without proper documentation and compliance, you may face steep consequences like tax evasion charges from the tax authorities.

This guide is for any company in the world that wants to hire internationally. Whether you’re a small business owner or hiring on behalf of a startup or enterprise, this guide will help you navigate how to hire independent contractors. Many sections address US companies, but many regulations and suggestions carry over to other countries.

Understand the difference between independent contractors and employees

The difference between employees and contractors isn’t always noticeable... but the distinction is legally and financially important Governments around the work keep an eye out for employment misclassification–more on that later.

But before you learn how to hire an independent contractor, take a moment to determine whether they actually qualify as an independent contractor. If you want to hire a web designer to create a new landing page for your corporate website, you want an independent contractor. That’s straightforward. But what if you want that person to provide consistent updates over several years? And what if you’re the only company they work for? The lines start to get blurry.

Who is an independent contractor?

Independent contractors are workers who offer their professional services to clients as a non-employee, usually on a project-based or fixed-term basis. They are self-employed, meaning they have a high degree of control over how and when they work. They are also responsible for paying self-employment taxes and do not receive statutory employee benefits from companies they work for. They typically (though not always) contract for multiple companies, working part-time and short-term for each.

Outside of the US, the terms of contractor relationships might vary slightly. But in the US, the IRS claims independent contractors have “the right to control or direct only the result of the work and not what will be done and how it will be done."

Employees are workers who receive statutory benefits and must complete work according to the company's preferences. When we say “must complete work according to the company's preferences,” we mean they attend mandatory onboarding training, meetings, and performance reviews.

In return, the company reimburses relevant expenses, provides tools, invests in employee learning and development, and offers paid vacation and benefits.

Check out our blog post on the difference between independent contractors and employees for further clarification.

Determine whether your independent contractor income is US-sourced

Another blurry line is whether income is US-sourced or not: do you follow the worker’s citizenship? The location of the worker? The location of the company? According to the IRS, the source of income paid to independent contractors is determined by the location where contractors perform the service. In other words, the independent contractor’s location determines where their income officially comes from, not the location of the company.

So even if a foreign independent contractor works for a US company, the income they receive is not US-sourced income as long as every aspect of the service occurs outside of the US. In that case, a US company should not withhold or report taxes. If a foreign independent contractor conducts any part of their services in the US, they must meet certain conditions to avoid tax obligation:

- The contractor was present in the US for no more than 90 days in a tax year

- The payment to the contractor is lower than $3,000

- The payment to the contractor is for services performed for an entity or office maintained in a foreign country

Not sure if you should classify a worker as an employee or independent contractor? Follow these three US tests for guidance.

Two other ways to hire foreign workers

If you know you want to hire foreign talent but aren’t tied to the idea of hiring an independent contractor, pause here. There are two other options you should know about: opening a local subsidiary and using a global PEO (or an EOR). Both of these options allow you to hire full-time employees abroad.

Opening a local subsidiary involves establishing a new legal entity in the foreign country, which hires the workers as local employees. You must set up local bank accounts, operating permits, and tax IDs, which involves substantial legal work.

Opening a local subsidiary can be efficient when a company plans to hire multiple workers in a particular country. For example, Amazon has a subsidiary called Amazon Canada to hire workers in Canada. But for most businesses, this setup is too complex, especially if they want to hire from multiple countries (and not just tap into one other country).

Partnering with an employer of record (or an international professional employer organization) is a better option for most companies because it’s less complex and allows you to hire in multiple additional countries. An EOR sets up local entities in countries around the world and then handles hiring and payroll services like employment contracts, international payroll, and employee benefits for your company. They ensure each of them complies with local laws of wherever you want to hire so you can spend your time focusing on other core business needs.

EORs technically hire employees on your behalf, which is what enables you to work with foreign employees legally without your own foreign subsidiary. This setup is not an option for hiring independent contractors: an EOR only hires full-time employees. (However, some companies that offer EOR services also give you the option. Learn how Deel helps you hire foreign employees and hire foreign independent contractors.)

People often use “international PEO” and "PEO" interchangeably. But international PEOs are much closer to EORs, which are quite different from regular PEOs. Learn about the differences in our guide on EOR vs. PEO.

Classify your independent contractors correctly

Once you understand that your new hire is indeed an independent contractor and have determined where in the world their income is sourced from, you have to ensure you classify them accordingly. Specifically, you must file the right documentation and treat them according to their classification. You may face charges for independent contractor misclassification if you fail to do so. Avoid misclassification at all costs: misclassification penalties are severe, sometimes reaching tens of millions in legal fees and back taxes.

The easiest way to check how to classify your employees is to use the IRS's 20 factor test. If you need additional clarification, you can ask the IRS to weigh in on the matter by completing Form SS-8 (Determination of Worker Status for Purposes of Federal Employment Taxes and Income Tax Withholding). The IRS may take at least six months to review your case and provide you with a determination.

Your best protection against misclassification (other than treating your independent contractors and employees appropriately) is to outline the relationship as precisely as possible in an independent contractor agreement. Don’t worry: we address independent contractor agreements below.

The classification process for foreign (non-US) independent contractors

As we already mentioned, each country’s federal laws determine the relationship between the payer and the service provider differently. Just because a person is a contractor in one country doesn't prove that they would be in another. When you hire an independent contractor internationally, take extra care to ensure they won't count an employee according to their local laws.

Each country has unique laws to determine whether someone should be considered an independent contractor, and many countries have revised their policies in recent years.

Some countries also require obtaining an independent contractor license, which can help with avoiding misclassification risks.

Some countries do not use the "independent contractor" and may use different terms and classifications, such as entrepreneur, auto-entrepreneur, sole-trader, freelancer, etc. Be sure to use the proper compliance documents based on the structure the worker has.

We go through these different requirements country-by-country in the local compliance section in our global hiring guide.

To ensure you are not at risk of misclassification, you may want to invest in local legal counsel that can help you determine how local laws interpret a working relationship. Also, check out our guide on what to do if a foreign contractor starts to resemble an employee to determine the best course of action.

Create a robust independent contractor agreement

A substantial written agreement is essential when hiring any contractor, especially a foreign one. A written contract will protect both you and the contractor from misunderstandings, ensure both parties hold up their end of the deal, and protect you against misclassification.

While free contract templates might sound like a time-saver, avoid using them. They usually don't have all the necessary elements and only apply to the laws of one country: they won’t be helpful in the case of a dispute.

There is no one-size-fits-all independent contractor agreement, so take time to create a contract that considers the local labor law regulations of both countries involved. Keep in mind that local regulations also determine the length of the contract, so periodically review it and revise if the scope of work has changed.

We have a detailed guide on how to write an independent contractor agreement. Essential elements to cover include:

- Scope of work describing the services offered by the independent contractor

- Compensation (and expenses if applicable)

- Classification and relationship of both parties, including the status of each party, liability, and indemnification clauses

- Ownership of work (considering local intellectual property laws, which vary from country to country)

- Confidentiality and data protection clauses (and a non-disclosure agreement clause if necessary)

- A non-compete clause that limits the contractor from working for a competitor within a certain number of days of the contract

- Termination and notice clauses outlining the duration of the contract

- Governing law clarifying which local laws apply should legal disputes arise

Building out a NDA agreement? Get our free template that we've annotated with notes tailored for remote and international teams.

Independent contractors are responsible for their own taxes. Companies that hire independent contractors do not need to worry about payroll taxes. The responsibility of reporting self-employment tax (and tax deductions) falls solely on the contractor. But depending on the contractor's country, the company is still responsible for compiling and reporting the total compensation on the appropriate tax slips.

File IRS Form 1099-NEC to report US-sourced income to the IRS

If your US-based company hired US-based contractors who earned more than $600 within a year, you need to report how much they earned by filing IRS Form 1099-NEC (Non-Employee Compensation) to the IRS each year. The deadline to file Form 1099-NEC is January 31 for the previous tax year.

On the 1099-NEC, report the total payments made during the year to any contractor that received more than $600. All four of these conditions must apply:

- Payment was made to someone who is not your employee

- Payment was made for services in the course of your trade or business

- Payment was made to an individual, partnership, estate, or, in some cases, a corporation

- Payment was made to that payee were at least $600 or more for the year

Note that the form changed in the tax year 2020. Form 1099-NEC replaces Form 1099-MISC for reporting payments to non-employees. Box 7 on Form 1099-MISC became Box 1 on Form 1099-NEC. Form 1099-MISC still exists but reports non-wage expenses such as rent payments. Read more about form 1099-NEC vs. form 1099-MISC on our blog.

Collect IRS form W-9 to keep track of 1099 (US) contractor information

US companies hiring American contractors request a IRS Form W-9 (Request for Taxpayer Identification Number and Certification) to collect tax information from their contractors.

Form W-9 lets employers collect the name, address, and social security number (or tax identification number, known as TIN) of the 1099 contractor in question. Remember: contractors working as business owners might give you their Employer Identification Number (EIN) instead. Employers only need to ask for a filled-out Form W-9 from contractors they paid more than $600 within a year. This form does not need to be submitted to the IRS since it is only a prerequisite for filling out Form 1099-NEC.

Collect IRS Form W-8BEN (or W-8BEN-E) for foreign independent contractors

The equivalent of the Form W-9 for foreign contractors is the IRS Form W-8BEN. It has two variations: Form W-8BEN for individuals and Form W-8BEN-E for foreign companies or self-employed workers operating under a business entity).

These forms certify that a person (or entity) is not, in fact, a US citizen. The hiring company is entitled to rely on the claims made on these forms to determine obligations regarding tax reporting and withholding. If you don't collect a W-8BEN from your contractor, you're obligated to withhold a 30% income tax from their pay.Every US company should have their foreign contractors complete this form. These forms are valid for three years. You must renew them if the working relationship continues longer than that. You can learn more about W-8BEN forms on the IRS' W-8BEN page.

Review how to hire independent contractors with different combinations of nationalities

It’s impossible to cover all the possible combinations of nationalities between companies and contractors in this blog post. That’s why we put together the global hiring guide. But here’s a quick recap of five common scenarios for US companies hiring independent contractors both locally and abroad.

US company hiring a US citizen living within the US

From the perspective of a US company, this is the most straightforward setup. The first step is to request the contractor to provide Form W-9. Each year, the company that hired the contractor will issue Form 1099-NEC by January 31 to report payments higher than $600 in the previous year. The company doesn't have to withhold any tax before paying the contractor. Remember, the company doesn't pay any payroll taxes, health insurance, workers' compensation insurance, or other FICA taxes (social security and medicare taxes).

US company hiring a US citizen living abroad

US citizens are subject to the same tax rules regardless of their location. The IRS will still consider an independent contractor as a US citizen if they perform the service abroad, even if the contractor is technically a tax resident of another country.

The company should continue to issue a Form 1099-NEC (given they paid the contractor more than $600 within a year), just like it would to its domestically-based US resident contractors. There are some cases where the tax implications change, so we advise you to take a look at IRS Publication 54, the Tax Guide for US Citizens and Resident Aliens Abroad, or consult their FAQ page about International Individual Tax Matters.

US company hiring a foreign independent contractor living abroad

The US company doesn't need to report the payments they made to the foreign independent contractor to the IRS if they are not US-sourced income. The company also doesn't need to withhold any tax. However, the company does need to collect W-8BEN(E) as proof of the contractor's status.

US company hiring a foreign independent contractor living in the US on a visa

First, the visa doesn’t determine tax status. The location where the independent contractor performs the services determines the source of the income. If the foreign contractor lives and delivers their services in the US, the income is US-sourced, and the company must withhold 30% as per non-resident tax rates.

However, these rules do not apply if a tax treaty exists between the countries (mentioned earlier in this article) or if a person becomes a resident.

In addition to withholding tax, the company needs to file Form 1042, Annual Withholding Tax Return for US Source Income of Foreign Persons, by March 15 of the following year. Some countries have a tax treaty with the US. Contractors from one of those companies should file Form 8233, Exemption From Withholding on Compensation for Independent (and Certain Dependent) Personal Services of a Nonresident Alien Individual.

How Deel provides visa support

Acquiring a visa for employees where you don’t own an entity can cost $200,000 and take months. We sponsor visas and hire the employee for you, so you don’t have to worry about payroll, taxes, and more.

See which visas your workers can obtain

![]()

US company hiring a Canadian independent contractor

Canada is one of the most popular countries for US companies to hire contractors because of the proximity and shared language and culture.

Suppose you hire a Canadian contractor to provide services to your company remotely. The additional rules and regulations come from the CRA (Canada Revenue Agency). Like its US counterpart, the IRS, the CRA imposes penalties for the misclassification of employees. But in cases where companies don't have a presence in Canada, penalties fall on the contractor.

You'll want to collect a W-8BEN form to waive the withholding tax from the contractor’s pay. You do not need to provide a Canadian independent contractor with a W-2 form at the end of the tax year because W-2 forms are for reporting employee compensation. You also do not need to provide a 1099-NEC because those are for US taxpayers. Of course, the independent contractor must report their income to the CRA.

One extra note: Citizens of Canada (and Mexico) are also allowed to work within the US temporarily without a visa. If a person makes US-sourced income as a non-resident, the hiring company will need to withhold 30% before payment is made and file a Form 1042 (Annual Withholding Tax Return for US Source Income of Foreign Persons). In the case of a tax treaty, Form 8233 (Exemption From Withholding) can be used to claim a tax exemption.

Read more about hiring and paying workers in Canada as a US employer.

Increase your protection with Deel Shield

Deel’s airtight contracts and advanced compliance features provide a great level of protection against misclassification risks. But if you want to eliminate any liability whatsoever — check out Deel Shield.

It’s our most secure level of contractor hiring to protect 100% from misclassification risks.

Enjoy full compliance when hiring independent contractors worldwide with Deel

It’s possible to hire and manage independent contractors across the world. But it’s complicated and risky. Deel provides a simple solution: we help companies worldwide work with global contractors and employees quickly and legally.

Our all-in-one solution provides:

- Contracts that are compliant with local labor laws

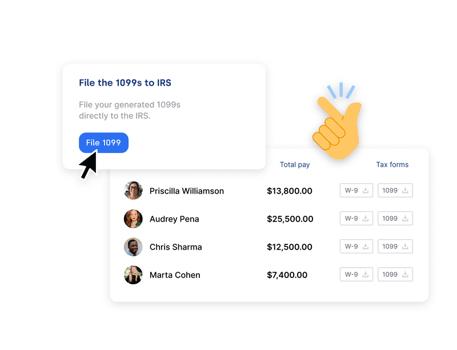

- Form collection and electronic filing with the IRS (W-9, W-9, W-8BEN, and 1099 forms)

- Global payroll, including multiple payment methods, local payouts, and currencies

- Compliance documentation to avoid misclassification risks worldwide

- Streamlined hiring of full-time employees and independent contractors (and simple conversion between the two)

Want to learn more about the easy way to hire and pay overseas workers? Book a demo today.

Disclaimer: This post is provided for informational purposes and should not be considered legal advice. Talk to a legal professional such as an employment lawyer for more info.

Join our monthly newsletter

The latest insights on today's world of work straight to your inbox.